The people of the UK are making extraordinary efforts to limit the health impact of Covid-19.

NHS staff, aided by carers and volunteers, are doing sterling work in the face of unprecedented pressures.

Families, friends, and neighbours are rallying round those who are ill or isolating themselves.

And thousands of businesses are safeguarding the well-being of their staff while ensuring essential supplies continue to flow to those who need them.

This crisis is very different from other economic shocks that the Bank has had to grapple with in the past.

That means it’s very difficult to judge how big the disruption is going to be or how long it’s going to last.

What is clear is that Covid-19 is already having a major impact on the UK economy.

This is borne out by the latest summary of business conditions compiled by me and my colleagues in the Bank’s network of agencies around the UK.

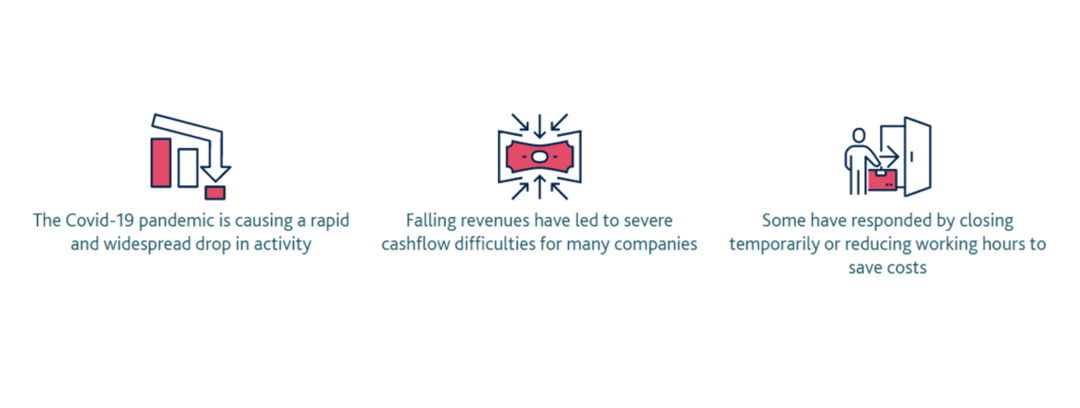

Our conversations with companies across the country indicate that households are spending much less, especially on travel and leisure, while staff absences, supply disruptions, and weak demand are leading to difficulties for businesses.

Unsurprisingly, many businesses have been putting their investment plans on hold and cancelling other spending.

All told, Covid-19 is causing a rapid and widespread fall in economic activity.

But if job losses and business failures can be limited, then the risk of lasting damage to the UK economy will be reduced.

That is why the Bank has been taking action over the past few weeks, putting in place a package of measures to help keep firms in business and people in jobs.

We have reduced Bank Rate from 0.75% to 0.10%, so that businesses and households can borrow more cheaply.

We have announced that £200 billion of new money will be injected into the economy (via quantitative easing, or QE) to boost spending and investment.

And we have introduced a new funding scheme (TFSME) which will provide banks with strong incentives to pass on the reduction in Bank Rate to customers and continue lending.

The TSFME is particularly targeted at incentivising lending to the small- and medium-sized businesses that often need more support at times like these.

In addition, we have reduced the amount of capital that banks have to hold in reserve against their lending. This should also serve to boost lending to businesses and households.

Having conducted ‘stress tests’ on the major banks and building societies late last year, we are confident that they are strong enough to keep lending, even in the face of a severe economic downturn.

The Bank is working closely with the Government to ensure our actions provide maximum support to the economy.

To support larger businesses in paying their staff and suppliers, the Bank and the Government have together introduced the Covid Corporate Financing Facility (CCFF), offering them cash in return for their corporate debt.

And the Government has announced its own substantial support measures. These include:

- options for businesses to defer VAT and PAYE payments;

- the Coronavirus Job Retention Scheme (CJRS), where employers can claim for 80% of the wages that they are paying staff who cannot work;

- the Self-Employment Income Support Scheme (SEISS) worth 80% of trading profits up to a maximum of £2,500 per month for 3 months;

- and the Coronavirus Business Interruption Loan Scheme (CBILS), from which small- and medium-sized businesses can borrow up to £5 million, with the Government giving guarantees to the banks that make those loans.

The unprecedented nature of the disruption means that the intelligence gathered by the Bank’s agents from their business contacts is crucial in ensuring our senior policymakers understand how Covid-19 is affecting Central Southern England and the rest of the UK.

We’re grateful to the many contacts who have been taking the time to give us this essential intelligence, despite the remarkable pressures they, their families, and their businesses are under.

With your help, my Bank colleagues and I will continue working to reduce the economic and financial impact of Covid-19 and to promote the good of the people of the UK.

Florence Hubert

Deputy Agent for Central Southern England at the Bank of England, @BoECentralSouth